Week 8: Decision Trees, Random Forests, Boosting and Gradient Boosting

Outline

Part 1: Motivation for Classification and Regression Trees

Part 2: Decision Trees

Part 3: Ensemble methods including Bagging, Random Forests, Boosting, Gradient Boosting, XGBoost

Geometry of Data for Classification

The decision boundary is defined where the probability of being in class 1 and class 0 are equal, i.e.

\[P(Y=1) = P(Y=0) \rightarrow P(Y=1) = 0.5\] - In logistic regression this is equivalent the log-odds=0: \(x\beta=0\)

Geometry of Data for Classification

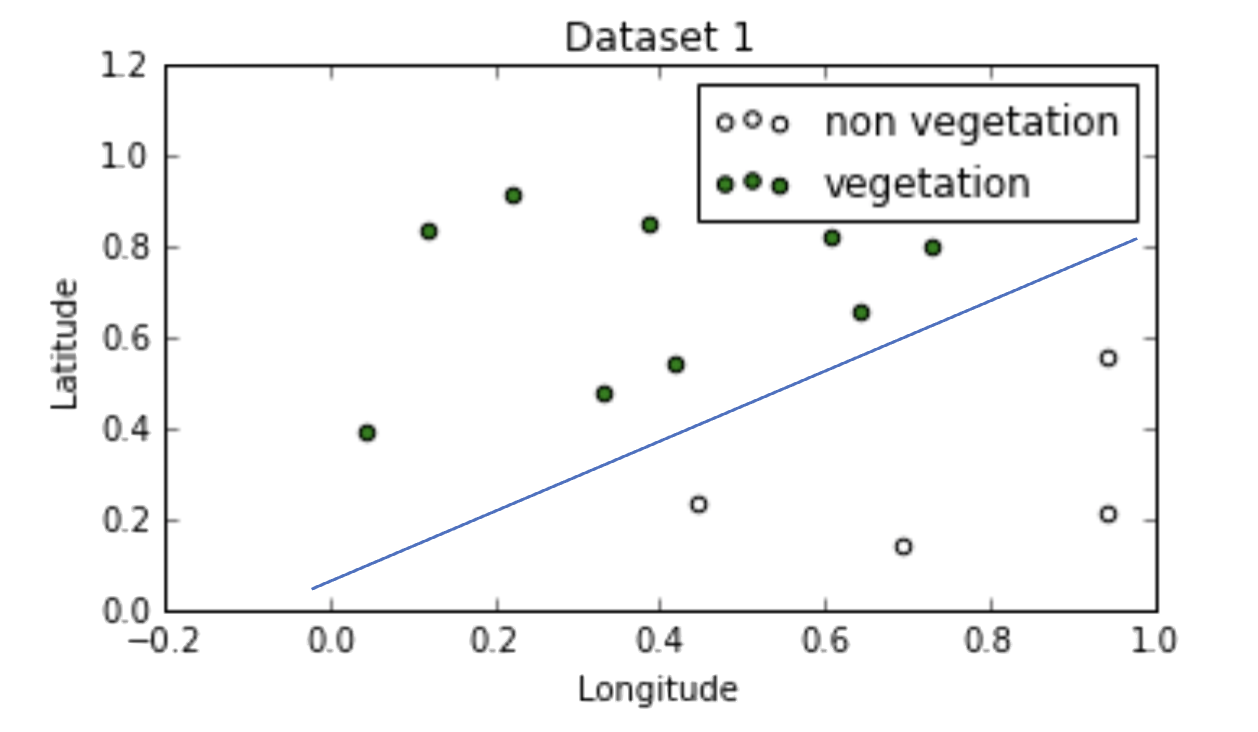

Here we are classifying vegetation and non-vegetation

The decision boundary is \[−0.8 x_1+x_2=0 \rightarrow x_2=0.8x_1\]

This translates to latitude \(=0.8\times\) longitude

Geometry of Data for Classification

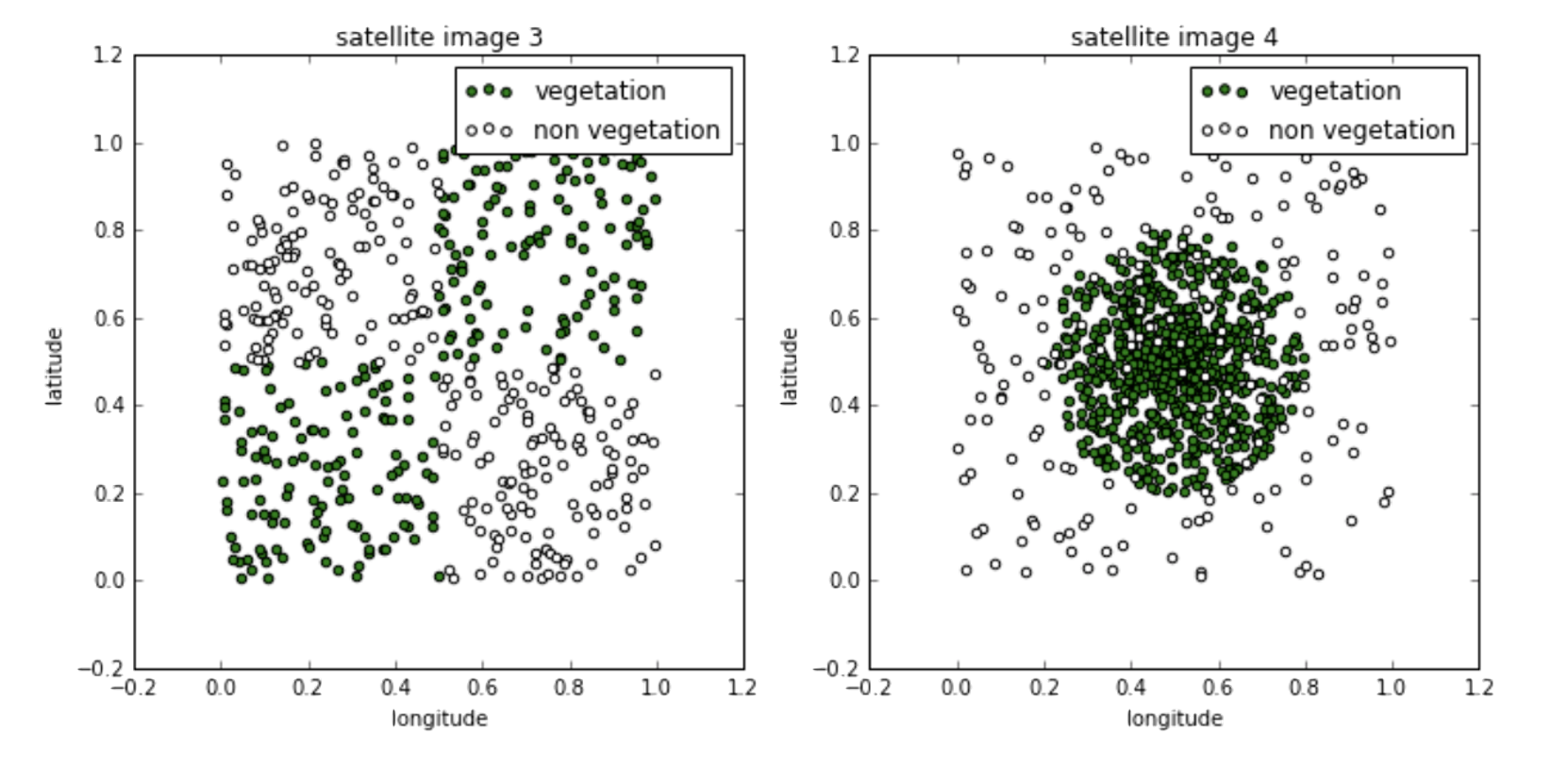

Logistic regression for classification works best when the classes are well separated in the feature space

Linear boundaries are easy to interpret, but not straightforward in non-linear cases

Geometry of Data for Classification

LHS: Multiple linear boundaries that form squares will perform better

RHS: Circular boundaries will perform better

Geometry of Data for Regression

In regression, the goal is to predict a continuous outcome rather than a class label

Instead of finding decision boundaries that separate classes, we partition the feature space into regions where we predict the mean response

Linear regression fits a global model: \(\hat y = x\beta\), which works well when the relationship is linear

But what if the relationship is non-linear or involves interactions?

We could add polynomial terms or interaction terms, but this requires knowing the form in advance

GAM models were a step in this direction

Tree-based methods automatically discover non-linear relationships and interactions by recursively partitioning the feature space

Regression Trees

A regression tree splits the feature space into \(M\) distinct, non-overlapping regions \(R_1, R_2, \dots, R_M\)

For each region, we predict the mean of the training responses in that region: \[ \hat y_{R_m} = \frac{1}{|R_m|} \sum_{i \in R_m} y_i \]

To build the tree, we minimize the residual sum of squares (RSS): \[\text{RSS} = \sum_{m=1}^{M} \sum_{i \in R_m} (y_i - \hat{y}_{R_m})^2\]

At each step, we choose the predictor \(j\) and split point \(s\) that minimize: \[\sum_{i: x_i \in R_1(j,s)} (y_i - \hat y_{R_1})^2 + \sum_{i: x_i \in R_2(j,s)} (y_i - \hat y_{R_2})^2\]

Decision Trees

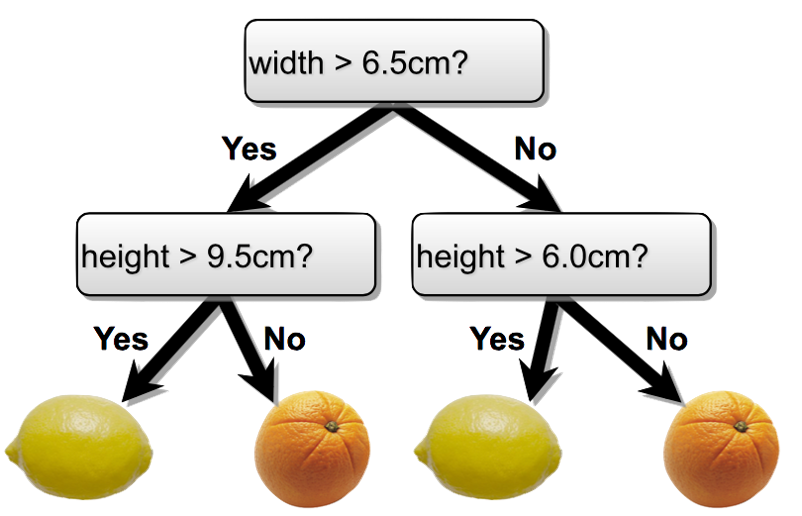

Simple flow charts can be formulated as mathematical models for both classification and regression.

Properties:

Interpretable by humans.

Sufficiently complex decision boundaries.

Locally linear decision boundaries.

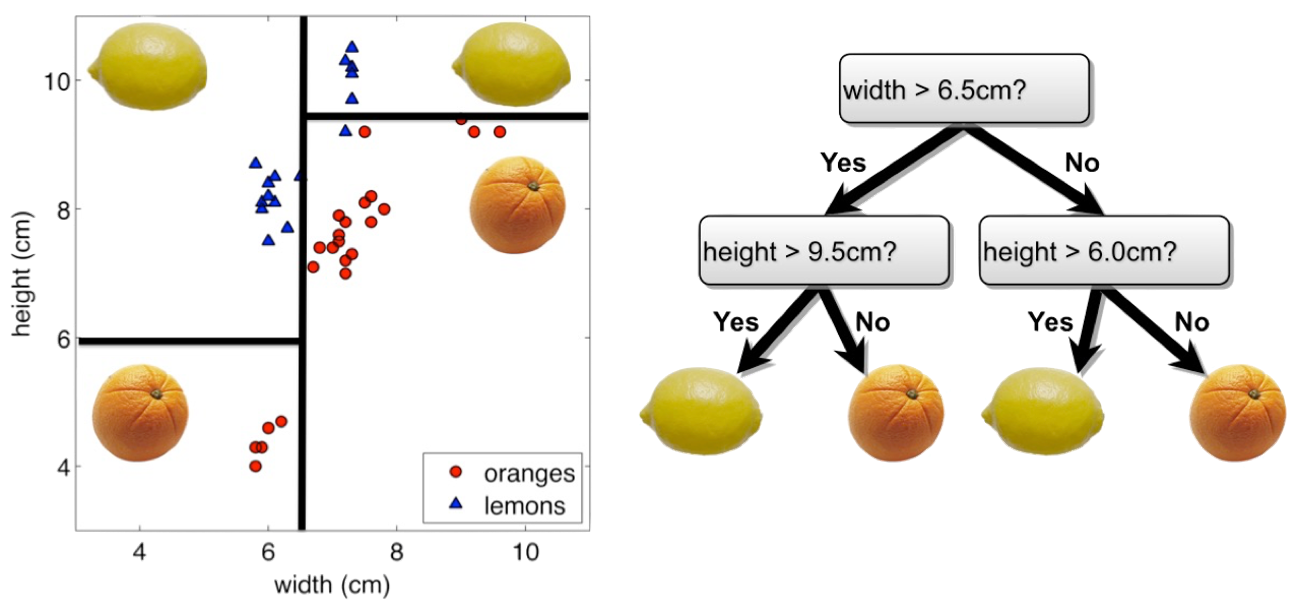

Decision Tree: Classification

Involve stratifying or segmenting the space into simple regions.

Decision Tree: Splitting

Formally, a decision tree model is one in which the final outcome of the model is based on a series of comparisons of the values of predictors against threshold values. Each comparison and branching represents splitting a region in the feature space on a single feature. Typically, at each iteration, we split once along one dimension (one predictor).

Decision Tree Terminology

Root node: the top of the tree — contains all observations before any split

Internal node: where a split occurs — applies a rule like “is \(x_j \leq t\)?” and sends observations left or right

Split: the act of dividing a node into two child nodes based on a feature and threshold

Leaf node (terminal node): where splitting has stopped — holds the final prediction

Classification: the majority class in that leaf

Regression: the mean response in that leaf

Depth: how many splits deep a node is from the root

Every path from root to leaf represents a series of if-then rules — this is what makes decision trees interpretable

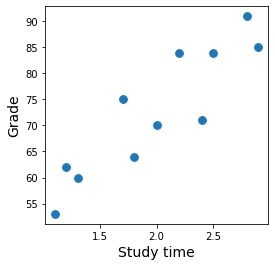

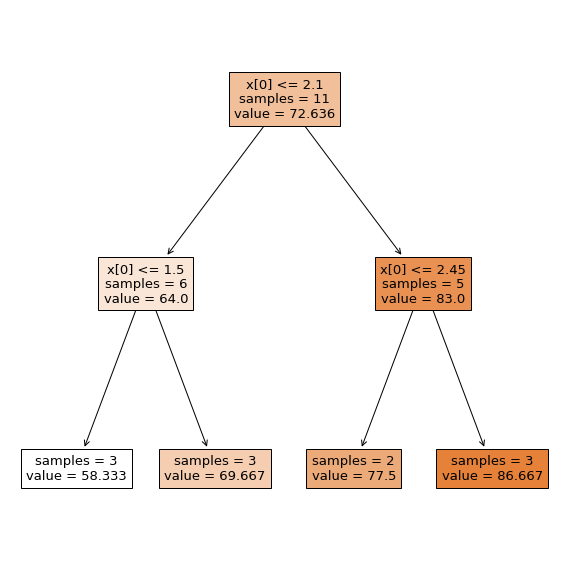

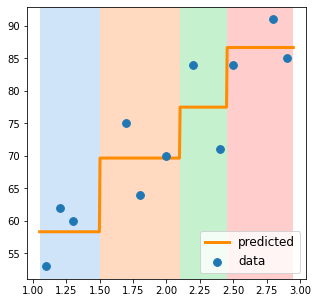

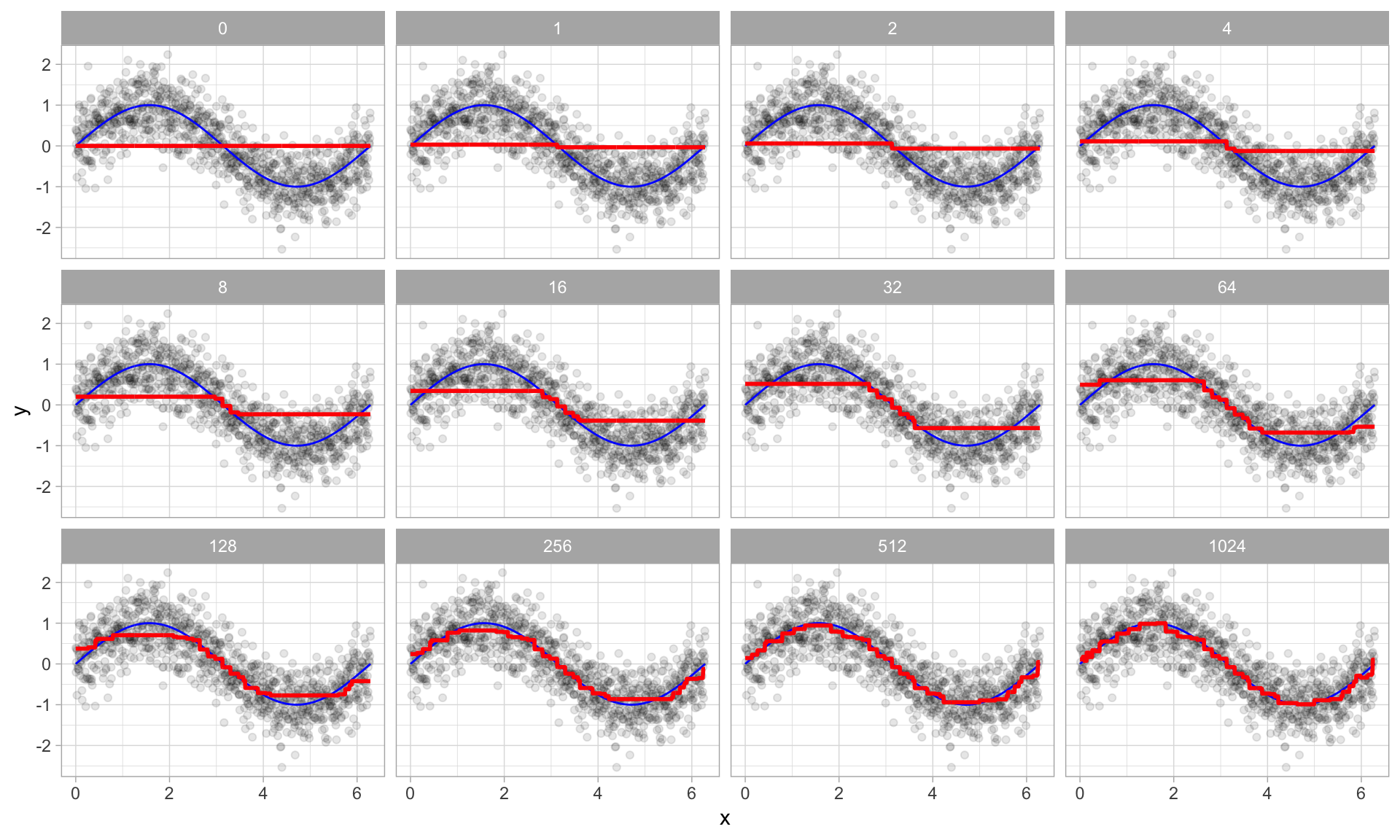

Decision Tree: Regression

Predict grade from study time

Decision Tree: Regression

The tree splits study time into \(M\) distinct, non-overlapping regions \(R_1, R_2, \dots, R_M\)

Learning the Tree Model

Start with an empty decision tree.

Choose the ‘optimal’ predictor and threshold for splitting.

Recurse on each new node until stopping condition is met.

Define the splitting criterion and stopping condition.

We need to define the splitting criterion and stopping condition

Greedy Algorithms

Always makes the choice that seems best at the moment.

Ensures local optimality at each step.

Makes greedy choices at each step to ensure that the objective function is optimized.

Never reverses a decision.

Example: Making change for $0.63

Available coins: quarters (25¢), dimes (10¢), nickels (5¢), pennies (1¢)

Greedy approach: always pick the largest coin that fits

25¢ → 25¢ → 10¢ → 1¢ → 1¢ → 1¢ = 6 coins

In decision trees: at each node, pick the single split (feature + threshold) that gives the best improvement — without considering whether a different split now might lead to a better tree overall

Optimality of Splitting

The greedy algorithm needs a metric to decide the “best” split at each node

No single ‘correct’ way to define an optimal split, but two common approaches:

Classification: minimize impurity — how mixed are the classes in each region?

Gini Index (most common), Entropy / Information Gain

Regression: minimize RSS — how far are observations from the region mean?

Common sense guidelines:

Feature space should grow progressively more pure (classification) or more homogeneous (regression) with splits

Fitness metric of a split should be differentiable

Avoid empty regions with no training points

Gini Index

The Gini Index is a metric used to measure the impurity or homogeneity of a dataset at a node.

It helps in determining the best feature to split on when building the tree.

Gini Index

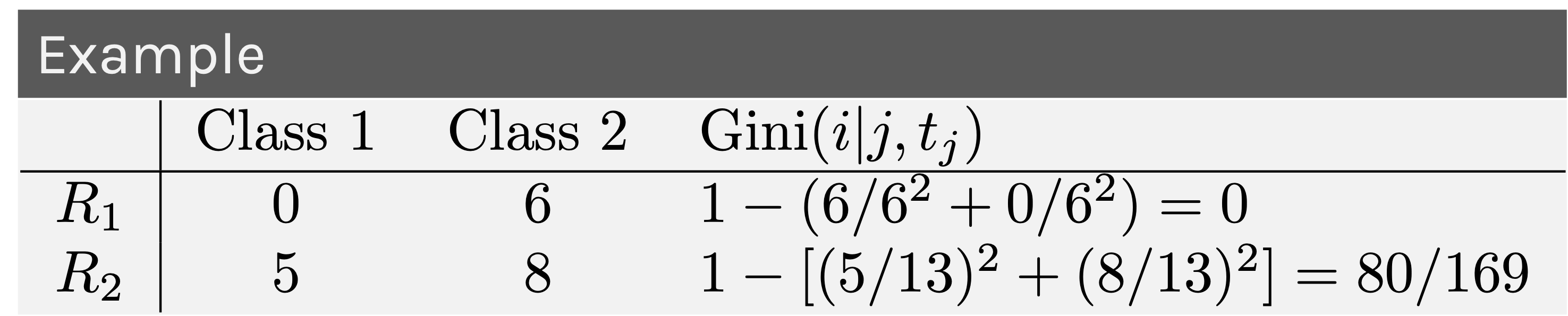

Suppose we have \(J\) predictors, \(N\) number of training points and \(K\) classes.

Suppose we select the \(j\)-th predictor and split a region containing \(N\) number of training points along the threshold \(t_j \in R\).

We can assess the quality of this split by measuring the purity of each newly created region, \(R_1,R_2\). This metric is called the Gini Index: \[Gini = 1 - \sum_{i=1}^{k} p(k|R_i)^2\]

Gini Index

Understanding Gini Index

If all samples at a node belong to the same class, Gini = 0 (pure node).

If samples are evenly distributed among classes, Gini is maximized.

The goal of splitting in decision trees (like CART) is to minimize the Gini Index, leading to purer nodes.

Gini Index

We can try to find the predictor \(j\) and the threshold \(t_j\) that minimizes the average Gini Index over the two regions, weighted by the population of the regions (\(N_i\) is the number of training points in region \(R_i\)):

RSS for Regression Trees

For regression, we use Residual Sum of Squares (RSS) instead of Gini

At each split, choose the predictor \(j\) and threshold \(s\) that minimize the weighted RSS across the two new regions:

where \(\hat y_{R_m}\) is the mean response in region \(R_m\)

Intuition: a good split creates regions where the observations are close to their region mean — i.e., the variation within each region is small

Like Gini, the greedy algorithm tries every feature and every possible split point, and picks the one with the lowest RSS

Splitting Criteria: Summary

Classification

Regression

Goal

Maximize purity

Minimize variance

Metric

Gini Index

RSS

Prediction

Majority class in region

Mean response in region

Greedy choice

Split that reduces Gini most

Split that reduces RSS most

From Splitting to Stopping

We now know how to evaluate a split: Gini (classification) or RSS (regression)

The greedy algorithm keeps splitting — but when should it stop?

If we never stop, the tree grows until every leaf contains a single observation

Perfect training accuracy, but massive overfitting

We need a stopping condition to decide when a split is no longer worth making

Gain: Measuring Improvement from a Split

Gain measures how much a split improves the metric — it is the difference between the impurity (or RSS) of the parent node and the weighted average of the children:

where \(m\) is the splitting metric (Gini, entropy, or RSS), \(R\) is the parent region, \(R_1, R_2\) are the child regions, and \(N_1, N_2\) are their sizes

High gain: the split meaningfully separates the data — worth doing

Low gain: the split barely improves things — may not be worth the added complexity

Zero gain: no improvement — the split does nothing useful

Stopping Conditions

We can stop splitting when:

The gain falls below a threshold — the split doesn’t improve enough to justify

A node reaches a minimum number of observations (e.g., min_samples_leaf)

The tree reaches a maximum depth

A node is already pure (Gini = 0) or has zero RSS

Problem: What is the major issue with pre-specifying a stopping condition?

You may stop too early (miss useful splits deeper in the tree) or too late (overfit)

Solutions:

Try several thresholds and cross-validate to find the best one

Or: don’t stop at all — grow the full tree, then prune it back

Pruning

Instead of trying to find the right stopping condition up front, grow a large tree first, then cut it back

A fully grown tree overfits — it memorizes the training data, including noise

Pruning: How It Works

Cost-complexity pruning: add a penalty for tree size

\[\text{Cost}(T) = \text{RSS}(T) + \alpha |T|\] - \(|T|\) = number of leaf nodes, \(\alpha\) = complexity parameter - Small \(\alpha\): keep more leaves (complex tree) - Large \(\alpha\): penalize leaves heavily (simpler tree)

For each \(\alpha\), find the subtree that minimizes Cost(\(T\))

Use cross-validation to choose the best \(\alpha\)

Pruning: Before and After

The pruned tree is simpler, more interpretable, and generalizes better to new data

We trade a small increase in training error for a large decrease in test error

Summary: Decision trees

Decision trees partition training data into homogenous nodes / subgroups with similar response values.

Pros

Decision trees are very easy to explain to non-statisticians.

Easy to visualize and thus easy to interpret without assuming a parametric form

Cons

High variance, i.e. split a dataset in half and grow tress in each half, the result will be very different

Related note - they generalize poorly resulting in higher test set error rates

But there are several ways we can overcome this via ensemble models

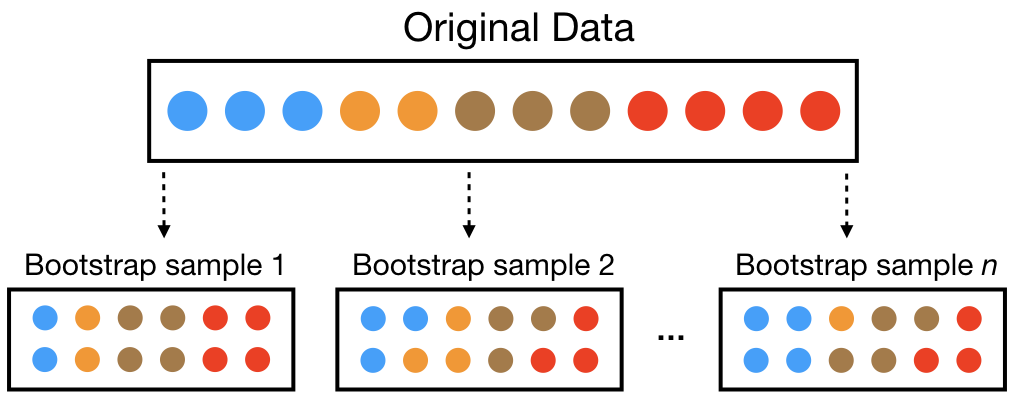

Bagging

Bootstrap aggregation (aka bagging) is a general approach for overcoming high variance

Bootstrap: sample the training data with replacement

Aggregation: Combine the results from many trees together, each constructed with a different bootstrapped sample of the data

Bagging Algorithm

Start with a specified number of trees \(B\):

For each tree \(b\) in \(1, \dots, B\):

Construct a bootstrap sample from the training data

Grow a deep, unpruned, complicated (aka really overfit!) tree

To generate a prediction for a new point:

Regression: take the average across the \(B\) trees

Classification: take the majority vote across the \(B\) trees

assuming each tree predicts a single class (could use probabilities instead…)

Improves prediction accuracy via wisdom of the crowds - but at the expense of interpretability

Easy to read one tree, but how do you read \(B = 500\)?

But we can still use the measures of variable importance and partial dependence to summarize our models

Random Forest Algorithm

Random forests are an extension of bagging

For each tree \(b\) in \(1, \dots, B\):

Construct a bootstrap sample from the training data

Grow a deep, unpruned, complicated (aka really overfit!) tree but with a twist

At each split: limit the variables considered to a random subset\(m_{try}\) of original \(p\) variables

Predictions are made the same way as bagging:

Regression: take the average across the \(B\) trees

Classification: take the majority vote across the \(B\) trees

Split-variable randomization adds more randomness to make each tree more independent of each other

Introduce \(m_{try}\) as a tuning parameter: typically use \(p / 3\) (regression) or \(\sqrt{p}\) (classification)

\(m_{try} = p\) is bagging

Example data: MLB 2021 batting statistics

The MLB 2021 batting statistics leaderboard from Fangraphs

We aim to predict WAR (Wins Above Replacement), an advanced metric that estimates the total number of wins a player contributes to their team compared to a “replacement-level” player. A replacement-level player is a theoretical player who is readily available, typically a Triple-A call-up or a minimum-salary free agent, and represents the baseline of a “0.0 WAR” player

import pandas as pdimport numpy as npmlb_data = pd.read_csv("http://www.stat.cmu.edu/cmsac/sure/2021/materials/data/fg_batting_2021.csv")mlb_data.columns = mlb_data.columns.str.lower().str.replace(" ", "_")# fix strings with % in BB% and K% to make numericfor col in ["bb%", "k%"]:if col in mlb_data.columns: mlb_data[col] = mlb_data[col].astype(str).str.replace("%", "").str.strip() mlb_data[col] = pd.to_numeric(mlb_data[col], errors="coerce")model_mlb_data = mlb_data.drop(columns=["name", "team", "playerid"], errors="ignore")model_mlb_data.head()

g

pa

hr

r

rbi

sb

bb%

k%

iso

babip

avg

obp

slg

woba

xwoba

wrc+

bsr

off

def

war

0

82

354

27

66

69

2

14.4

17.2

0.336

0.346

0.336

0.438

0.671

0.462

0.439

194

0.2

40.9

-7.5

4.6

1

68

288

27

66

58

18

12.5

28.1

0.395

0.333

0.302

0.385

0.698

0.443

0.420

185

5.4

35.7

-3.2

4.2

2

79

347

16

61

52

0

13.5

17.0

0.231

0.324

0.298

0.398

0.529

0.397

0.377

157

-2.7

21.6

5.7

4.0

3

82

372

21

63

54

10

8.9

23.9

0.256

0.329

0.286

0.349

0.542

0.379

0.328

139

1.0

18.7

5.4

3.7

4

78

342

23

67

51

16

13.2

24.3

0.313

0.306

0.278

0.386

0.592

0.409

0.428

159

2.7

27.6

-2.2

3.7

MLB 2021 Batting Statistics: Variables

Column

Description

Column

Description

g

Games played

babip

Batting avg on balls in play

pa

Plate appearances

avg

Batting average

hr

Home runs

obp

On-base percentage

r

Runs scored

slg

Slugging percentage

rbi

Runs batted in

woba

Weighted on-base average

sb

Stolen bases

xwoba

Expected wOBA (Statcast)

bb%

Walk rate (%)

wrc+

Weighted runs created plus

k%

Strikeout rate (%)

bsr

Base running runs above avg

iso

Isolated power (SLG − AVG)

off

Offensive runs above avg

def

Defensive runs above avg

Target: war — Wins Above Replacement. Note, off, def, and bsr are direct components of WAR (WAR is approx Off + Def + BsR + replacement adjustment).

Example Random Forest

scikit-learn’s RandomForestRegressor is a popular implementation

Each bootstrap sample draws \(N\) observations with replacement from the original \(N\)

Some observations will be selected multiple times, others not at all

On average, about \(63\%\) of observations end up in any given bootstrap sample

The remaining \(\approx 37\%\) are called out-of-bag (OOB) observations for that tree

For each observation \(i\), roughly \(B/3\) trees were built without seeing it

We can predict observation \(i\) using only those trees — giving a built-in test set estimate without needing cross-validation

OOB: Why 63%?

The probability that observation \(i\) is not selected in a single draw is \(\left(1 - \frac{1}{N}\right)\)

After \(N\) draws with replacement: \(P(\text{not in sample}) = \left(1 - \frac{1}{N}\right)^N \approx e^{-1} \approx 0.368\)

So \(P(\text{in sample}) \approx 1 - 0.368 = 0.632\), i.e. about \(63\%\)

This means each tree has a free validation set of ~37% of the data

The OOB error is computed by aggregating predictions for each observation using only the trees that did not include it in training

OOB in the MLB example

# Refit with oob_score=True to get OOB R²oob_rf = RandomForestRegressor(n_estimators=50, oob_score=True, random_state=42)oob_rf.fit(X, y)print(f"R² (training): {oob_rf.score(X, y):.4f}")print(f"R² (OOB): {oob_rf.oob_score_:.4f}")

R² (training): 0.9876

R² (OOB): 0.9144

The training R² is high because the model has seen this data

The OOB R² is a more honest estimate of performance on unseen data.

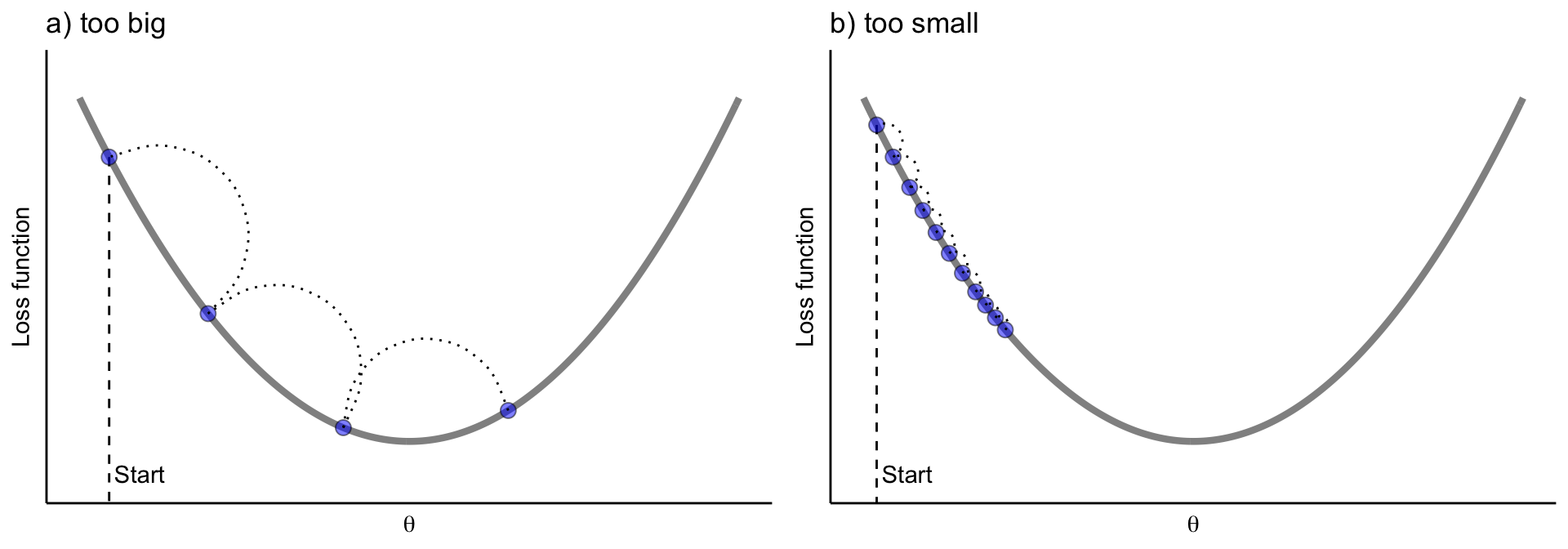

Tuning Hyperparameters

A model’s hyperparameters are settings chosen before training — they control how the model learns, not what it learns

Default values often work reasonably well, but tuning can significantly improve performance

Under-tuned model: may underfit (too simple) or overfit (too complex)

Well-tuned model: finds the sweet spot between bias and variance

Tuning is done via cross-validation: try different hyperparameter values, evaluate each on held-out folds, and pick the combination that generalizes best

This is especially important for ensemble methods where multiple hyperparameters interact with each other

Random Forest Hyperparameters

Parameter

scikit-learn

What it controls

Number of trees

n_estimators

More trees = more stable predictions, but slower

Features per split

max_features

Most important: controls \(m_{try}\), the randomness at each split

Max tree depth

max_depth

How deep each tree can grow (limits complexity)

Min samples to split

min_samples_split

A node must have at least this many observations to be split

Min samples in leaf

min_samples_leaf

Each leaf must contain at least this many observations

Bootstrap

bootstrap

Whether to use bootstrap sampling (True) or full dataset (False)

Max leaf nodes

max_leaf_nodes

Cap on total number of leaves per tree

max_features is the most important — it controls the bias-variance tradeoff

Small max_features: trees are more different (less correlated), but individually weaker

Large max_features: trees are stronger individually, but more similar to each other

Rule of thumb: \(p/3\) for regression, \(\sqrt{p}\) for classification

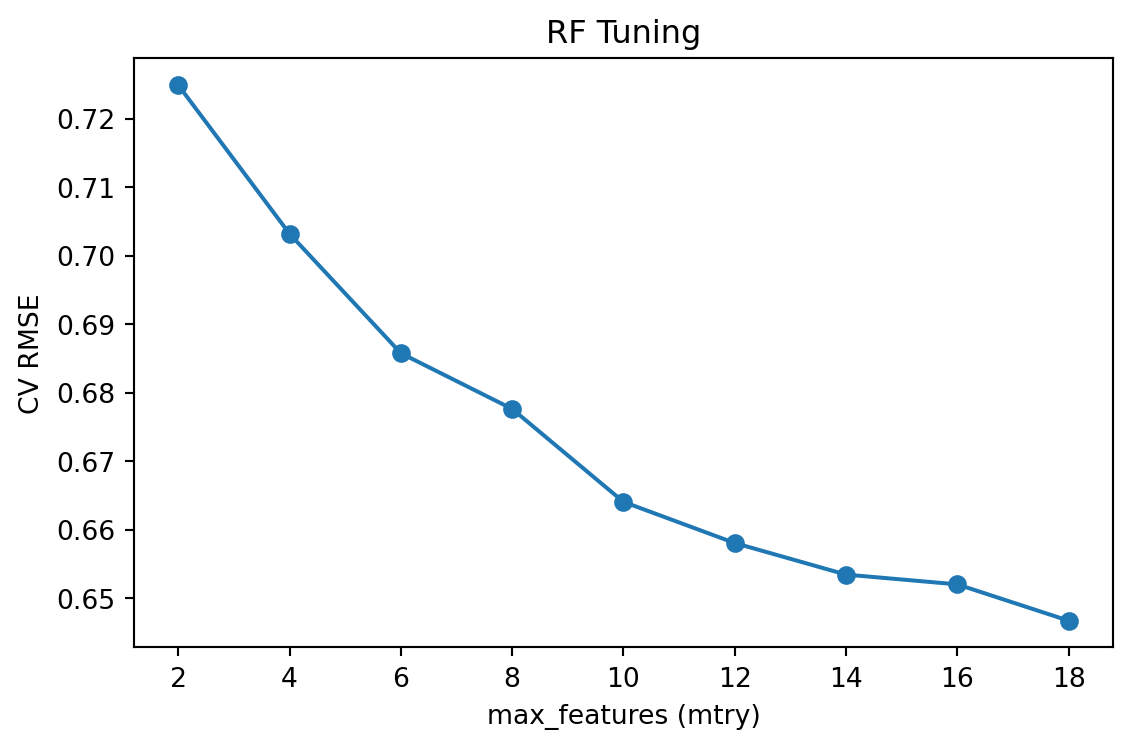

Tuning Random Forests

Important: max_features (equivalent to \(m_{try}\))

Marginal: tree complexity, splitting rule, sampling scheme

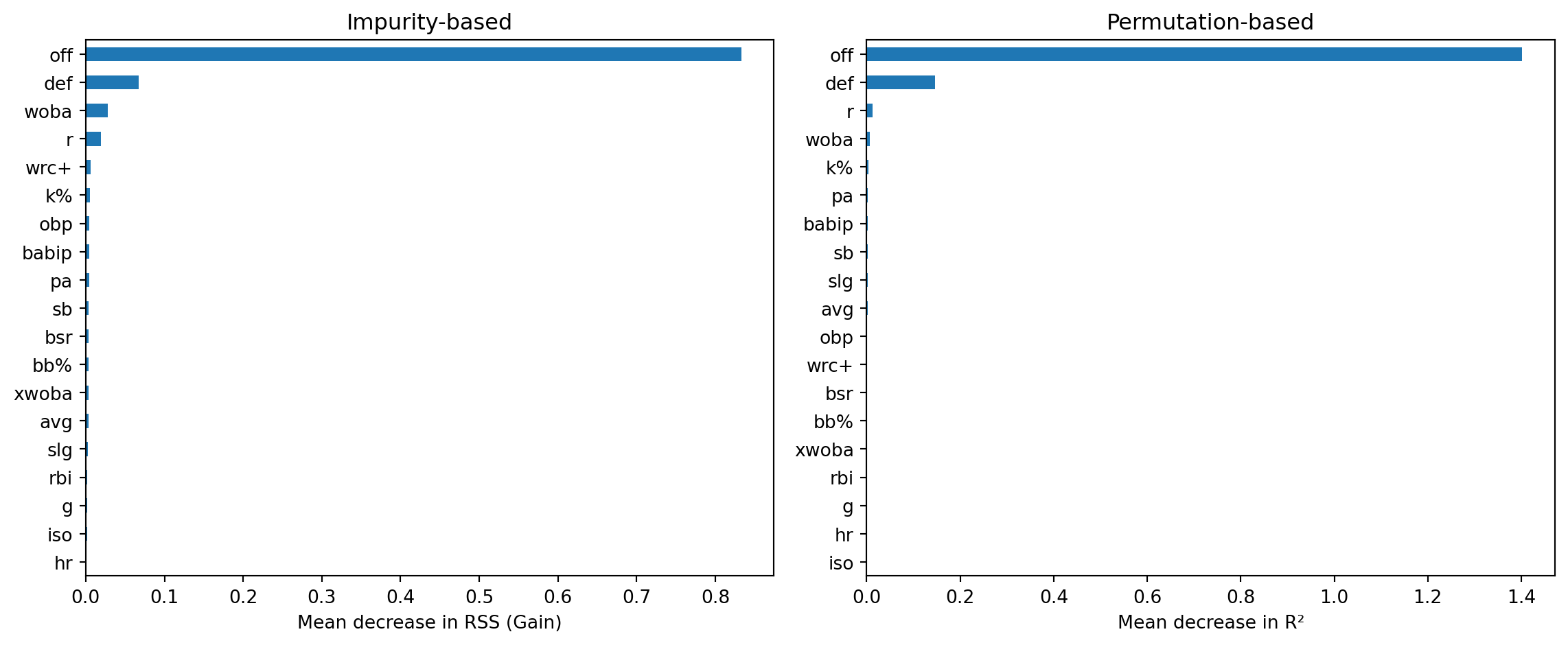

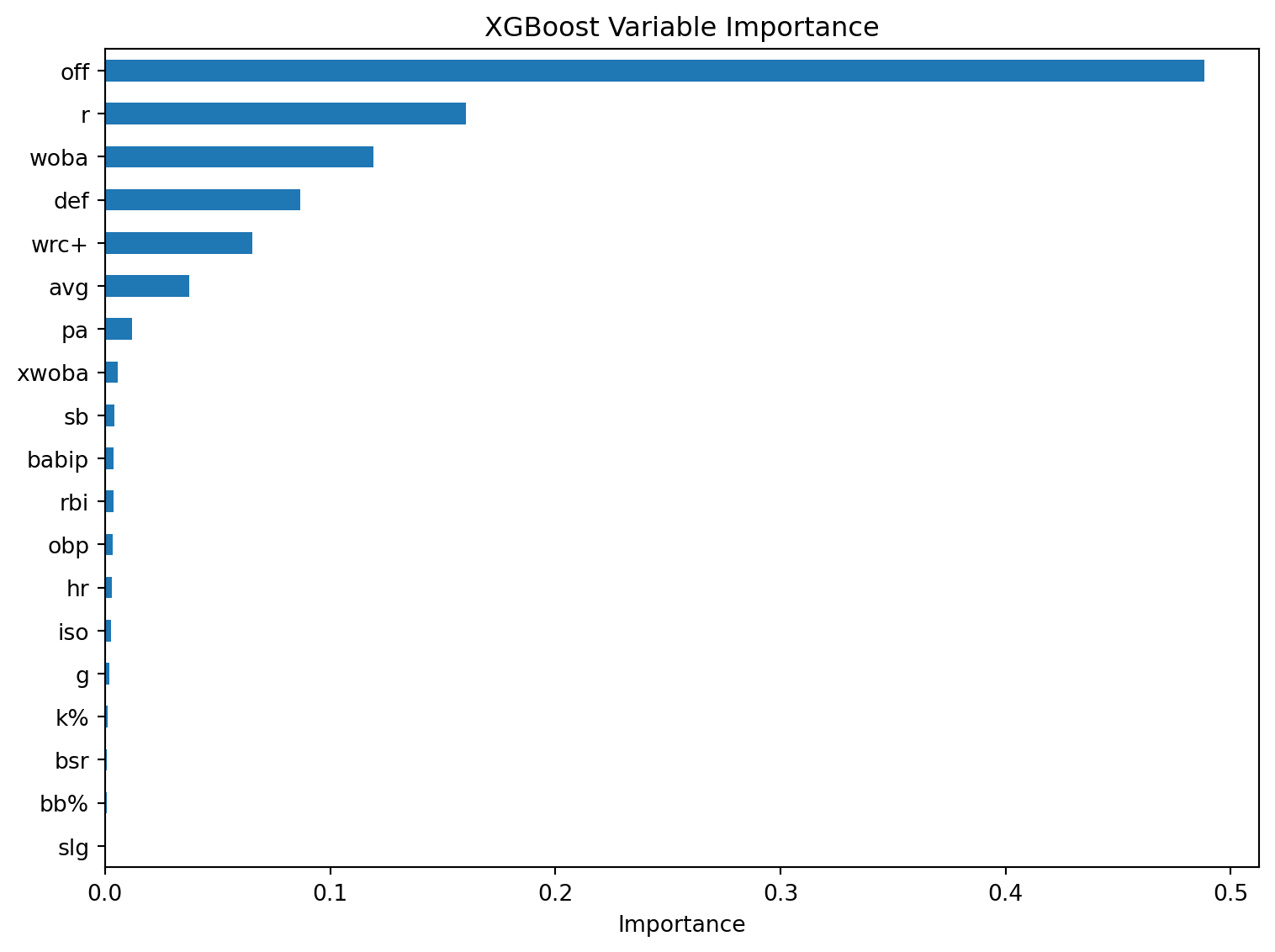

After fitting a random forest, we want to know: which features matter most?

Two common approaches:

Impurity-based (Gain): total reduction in the splitting criterion (e.g. RSS for regression, Gini for classification) each time a feature is used to split, averaged over all trees

Permutation-based: randomly shuffle one feature’s values and measure how much the model’s accuracy drops — bigger drop = more important

Impurity-based importance is fast (computed during training) but can be biased toward high-cardinality features

Permutation importance is more reliable but slower (requires re-prediction)

Variable Importance: MLB Example

from sklearn.inspection import permutation_importance# Impurity-based (gain)gain_imp = pd.Series( oob_rf.feature_importances_, index=X.columns).sort_values(ascending=True)# Permutation-basedperm = permutation_importance( oob_rf, X, y, n_repeats=10, random_state=42)perm_imp = pd.Series( perm.importances_mean, index=X.columns).sort_values(ascending=True)fig, axes = plt.subplots(1, 2, figsize=(12, 5))gain_imp.plot.barh(ax=axes[0])axes[0].set_xlabel("Mean decrease in RSS (Gain)")axes[0].set_title("Impurity-based")perm_imp.plot.barh(ax=axes[1])axes[1].set_xlabel("Mean decrease in R²")axes[1].set_title("Permutation-based")plt.tight_layout()plt.show()

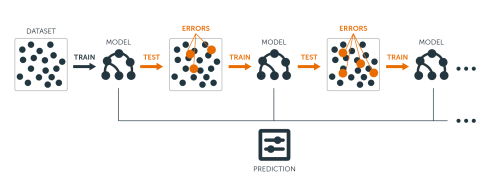

Boosting

Build ensemble models sequentially

start with a weak learner, e.g. small decision tree with few splits

each model in the sequence slightly improves upon the predictions of the previous models by focusing on the observations with the largest errors / residuals

Boosted trees algorithm

Write the prediction at step \(t\) of the search as \(\hat y_i^{(t)}\), start with \(\hat y_i^{(0)} = 0\)

Fit the first decision tree \(f_1\) to the data: \(\hat y_i^{(1)} = f_1(x_i) = \hat y_i^{(0)} + f_1(x_i)\)

Fit the next tree \(f_2\) to the residuals of the previous: \(y_i - \hat y_i^{(1)}\)

Add this to the prediction: \(\hat y_i^{(2)} = \hat y_i^{(1)} + f_2(x_i) = f_1(x_i) + f_2(x_i)\)

Fit the next tree \(f_3\) to the residuals of the previous: \(y_i - \hat y_i^{(2)}\)

Add this to the prediction: \(\hat y_i^{(3)} = \hat{y}_i^{(2)} + f_3(x_i) = f_1(x_i) + f_2(x_i) + f_3(x_i)\)

Continue until some stopping criteria to reach final model as a sum of trees:

\[\hat{y_i} = f(x_i) = \sum_{b=1}^B f_b(x_i)\]

Visual example of boosting in action

Gradient boosted trees

Regression boosting algorithm can be generalized to other loss functions via gradient descent - leading to gradient boosted trees, aka gradient boosting machines (GBMs)

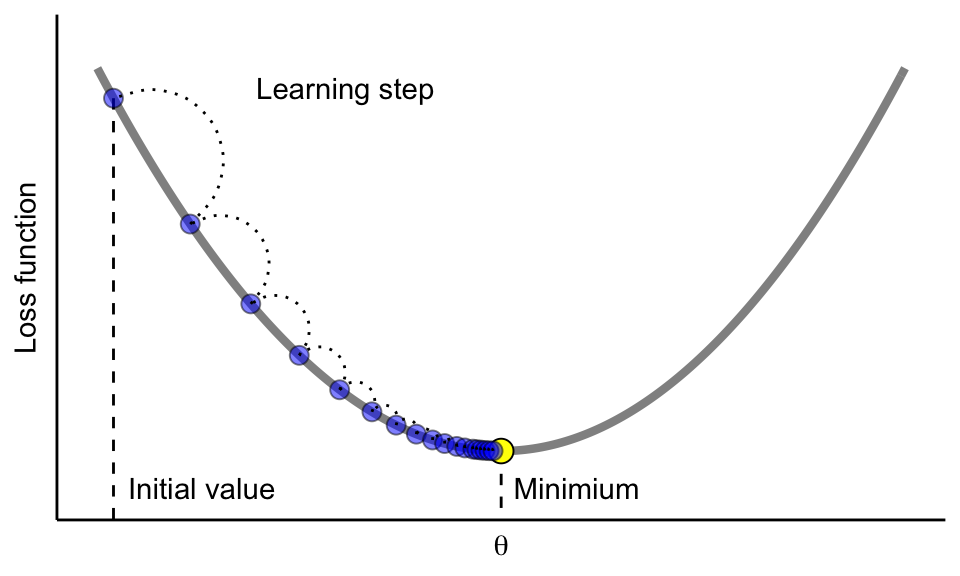

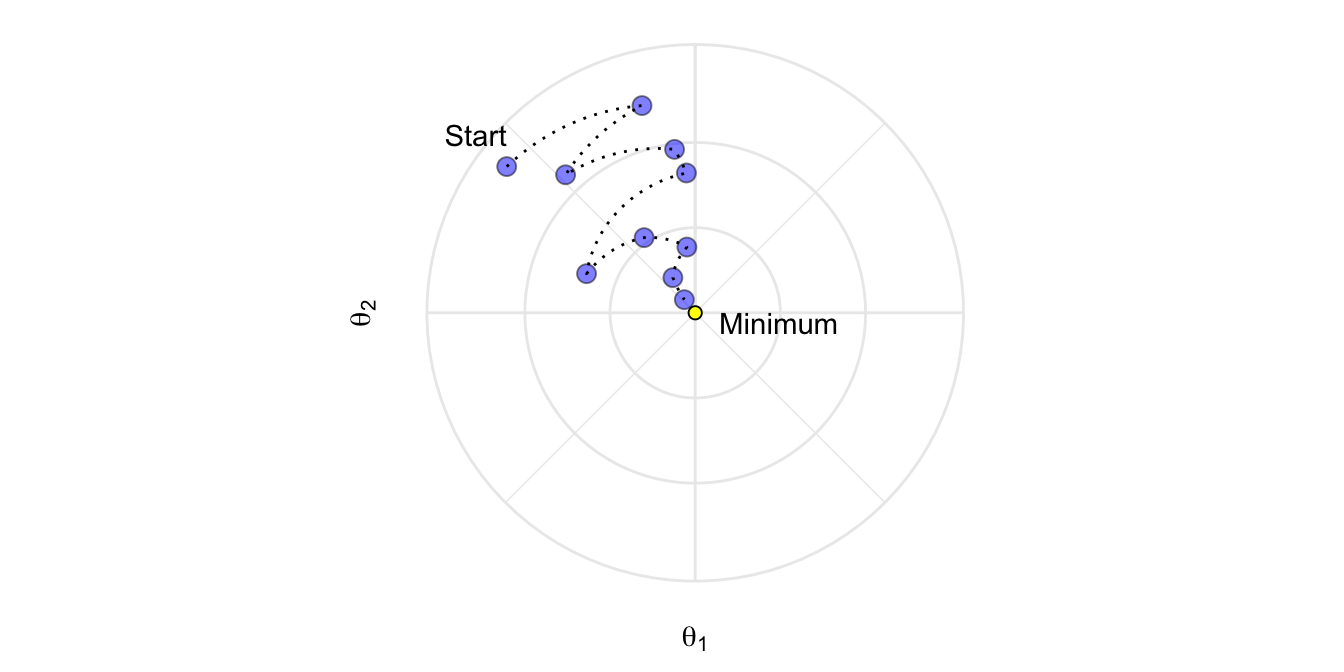

Update the model parameters in the direction of the loss function’s descending gradient

Tune the learning rate in gradient descent

We need to control how much we update by in each step - the learning rate

Stochastic gradient descent can help with complex loss functions

Batch gradient descent computes the gradient using all\(N\) observations — expensive, and can get stuck in local minima

Stochastic GD randomly samples a subset of data each iteration

The gradient estimate is noisier, which actually helps:

Escape local minima and saddle points

Each update is cheaper to compute

Adds a regularization effect — noisy updates prevent overfitting

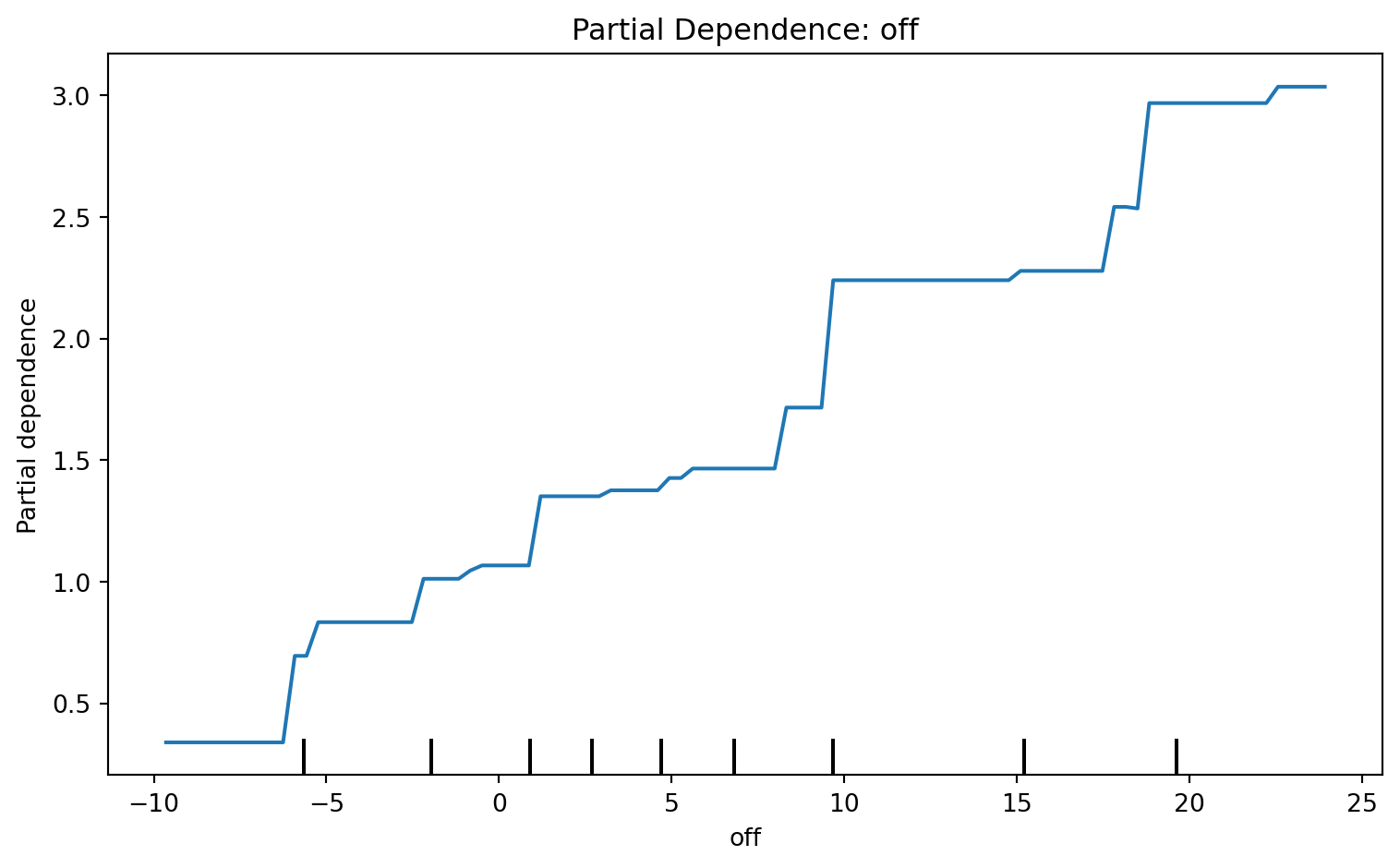

Variable importance tells us which features matter, but not how they affect predictions

Partial dependence plots show the marginal effect of a feature on the predicted outcome

How it works: for a feature \(x_j\), evaluate the model at each value of \(x_j\) while averaging over all other features: \[\hat{f}_j(x_j) = \frac{1}{N} \sum_{i=1}^{N} \hat{f}(x_j, \, x_{i,-j})\]

Flat line → feature has little effect on predictions

Steep slope → predictions are sensitive to that feature

Non-linear shape → model learned a relationship that linear regression would miss

PDPs work with any model (random forests, GBMs, etc.), not just XGBoost

Partial Dependence: MLB Example

This is the partial dependence parameter for the off variable